Interest rates have decreased globally. Even StashAway has decreased its projected rate for StashAway Simple to 1.4% p.a. Is there even a savings plan right now that offers above 2% base p.a.? Yes, for now. Singlife is kind of the answer to that question. And the $5 (up to $35) Singlife referral bonus/promo code is something not to be missed! ($5 bonus sign-up link here)

Let us explore whether Singlife is a good insurance savings plan for you.

Singlife Referral Bonus Gives You $5 Upfront

You will get $5 credited into your account upon signing up – Yes, free bonus money!

Singlife Referral Bonus 2021

To qualify for the $5 bonus:

1. Download the app + sign up with our link on your mobile

2. Request for a Singlife Visa Debit Card (FREE) on the app

3. Activate the card once received

Bonus: Extra $35 if you sign up for Singlife’s Grow.

To enjoy the $5 bonus, download the app and sign up using our link here on your mobile phone.

Disclaimer

This article here is for reference purposes and must not be taken as any form of business, legal, investment or taxation advice. It, in no way, represents or constitutes an offer or solicitation to purchase any investment.

Keep in mind that this content is not financial advice from a professional. If you are doubtful or unsure as to the action you should take, please consult a professional.

This article contains affiliate links and we may receive a commission from your sign-ups.

What is Singlife?

Remember feeling like you’re putting money into a bottomless pit when you pay your monthly insurance premiums?

That’s the feeling of a traditional insurance policy: most of your premiums are expensed as distribution costs (e.g. commissions for your agent) for a good 5-10 years.

Image Source: Freepik

Breaking even would take even longer, so surrendering a bad policy such as the one purchased by your parents is usually not a feasible thing to do while you’re young.

‘It’s not worth it.’

So they said.

Singlife takes that feeling away.

When depositing funds into Singlife, the principal amount is retained 100% as there are zero distribution costs; the policies are purchased without financial advice.

Surrendering an insurance policy has never been this smooth and quick, and this will prove useful to help you make it through rainy days like the COVID-19 pandemic.

Of course, the high amount of flexibility does come with some trade-offs, but Singlife remains an excellent insurance alternative to your personal risk management strategy.

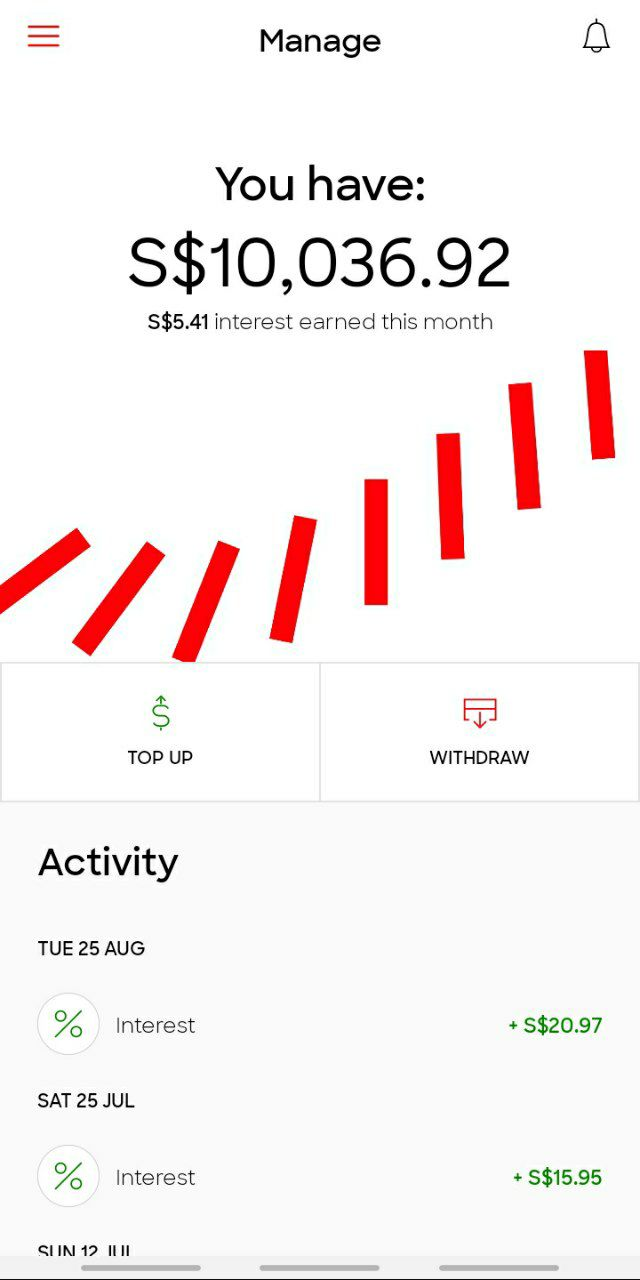

High Teaser Interest Rates – 2.5% P.A. for the first $10,000 SGD!

Here comes the most attractive part about SingLife, the high-interest rate that your bank or fixed deposit can’t provide you anymore!

You will enjoy a 2.5% (2% from 1st November 2020 onwards) per annum interest rate for the first $10,000SGD deposited and a 1% rate for the next $90,000SGD. No interest will be earned on the account value when your daily account value is less than the prevailing minimum account value or on the amount above $100,000 SGD.

Update: Singlife will be adjusting their crediting rates on the Singlife Account from 2.5% to 2% per annum (p.a.) for the first S$10,000 with effect from 1 November 2020. The return continues to remain competitive with no lock-ins or withdrawal fees. There will also be no change to the 1% p.a. return for the next S$90,000 in the Singlife Account.

Update (Again): In view of current market conditions, Singlife will be adjusting its crediting rate (return) on the Singlife Account from to 1.0% per annum (p.a.) for the first S$10,000 with effect from July 2021.

The interest will be calculated daily and only credited to you at the end of the month.

While it provides a higher interest rate than many others, it is neither a bank account nor a fixed deposit, the returns are not guaranteed.

But it offers the flexibility of withdrawing your money via FAST transfer or by using your Singlife Visa Debit card any time so this gives you an option to park your excess cash or savings.

“Save, Spend, Earn” Campaign

To unlock even more rewards, customers can stack their returns to receive up to 2.0% in total returns p.a. on the first S$10,000 by:

- Participating in the “Save, Spend, Earn” campaign, now extended to 31 December 2021, to enjoy an additional 0.5% return p.a. on the first $10,000 in their Singlife Account.

- Signing up for a Grow policy and kickstart with a minimum amount of S$1,000 to enjoy an additional 0.5% return p.a. on the first $10,000 in their Singlife Account.

Singlife Visa Debit Card

Please be reminded that to qualify for the bonus referral of $10, you should fund the minimum amount of $500 and order your SingLife Visa Debit Card via the app.

This is absolutely complimentary.

As advertised by them, this card can be used worldwide with no additional FX fees and zero annual fees. Something like your multi-currency YouTrip and TransferWise card.

Of course, while making an overseas purchase, do remember to pay in the original currency as much as possible to reap the most FX fees benefit.

No Lock-ins or Fees

As mentioned previously, you may access and withdraw your money at any time from your Singlife Account policy without any penalty.

This is something worth mentioning since the flexibility allows you to retain high liquidity although you have put a sum into insurance; unlike other traditional insurance plans, where the insured may only rely on unfavourable coupons payouts.

Easy to Use App – Although A Lil’ Glitchy

It is a great app with an easy-to-use interface but it could get a bit buggy at times.

Instances like that above have occurred multiple times.

But all in all, it is a VERY simple app with minimal functions that serves its purpose.

You would only be checking your returns occasionally and doing a one-time order of your debit card on your app.

So the app being buggy at times isn’t that much of a concern here.

Insurance Benefits for Singlife Accounts

Image Source: Freepik

At first glance, this new insurtech sure has quite a few unique things to offer. Things that ordinary life policies would not be able to offer.

But there’s more than meets the eye.

Singlife gives you the option of withdrawing (aka no lock-ins) and surrendering at any time, but they would have the ability to terminate or change the terms and conditions of your policy with a 90 days notice.

Think about the times when agents were fear-mongering you to purchase insurance policies because the countdown to a certain critical illness definition change has begun. This won’t matter anymore since your policy definitions are not fixed anyways.

Guess you can’t have the best of both worlds in this case!

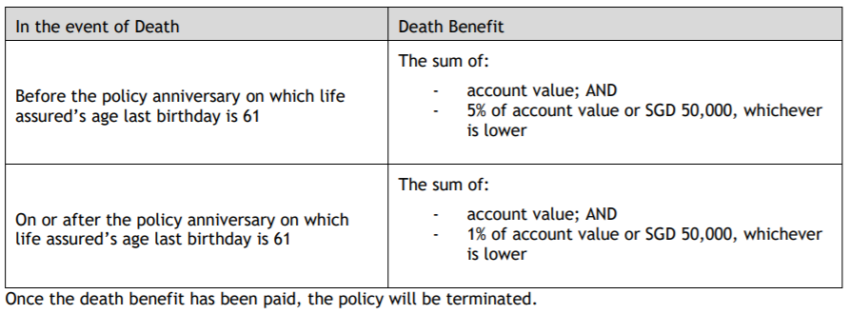

Pooled Death Benefit/Critical Illness Benefit

As understood from the policy terms, the coverage for death and critical illness or terminal illness are pooled together.

That means once either benefit is received, the policy will cease to exist, i.e. terminated.

The benefit is also defined as 105% and 101% of the account value for policy anniversary before the age of 61 and after 61 respectively. The 5% or 1% coverage is subjected to a 50,000 SGD cap as well, whichever is lower.

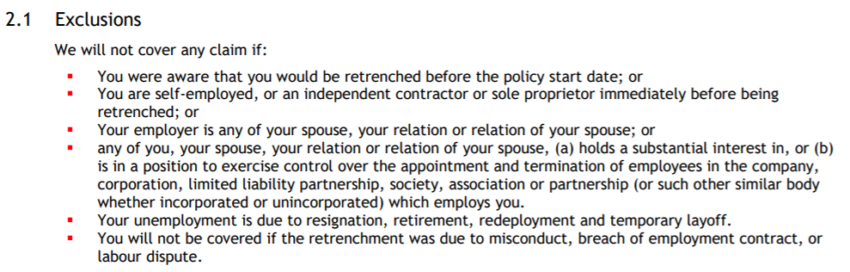

Retrenchment Benefits: Not So Straightforward, But Better Than Nothing!

Image Source: Freepik

As understood from the policy terms, the coverage for retrenchment is a tad harder to claim.

In essence, the insured must remain unemployed for at least 4 months and the attained age at renewal is fifty-five (55) or below.

The retrenchment benefit can only be claimed once, calculated based on the average card transaction for the last 6 months before retrenchment, and paid over 3 months.

There are several exclusions in place to prevent users from ‘gaming the system’ as well.

Not the usual Deposit Insurance Scheme

Heated debates, bold assumptions and vague descriptions.

Singlife is believed to be a registered member under the Policy Owners’ Protection Scheme administered by the Singapore Deposit Insurance Corporation (SDIC).

Although protected by SDIC, Singlife is not covered under the usual deposit insurance scheme that we are accustomed to like the rest of the banks and Robo advisors in Singapore.

Your Singlife account is protected Policy Owners’ Protection (PPF) Scheme instead.

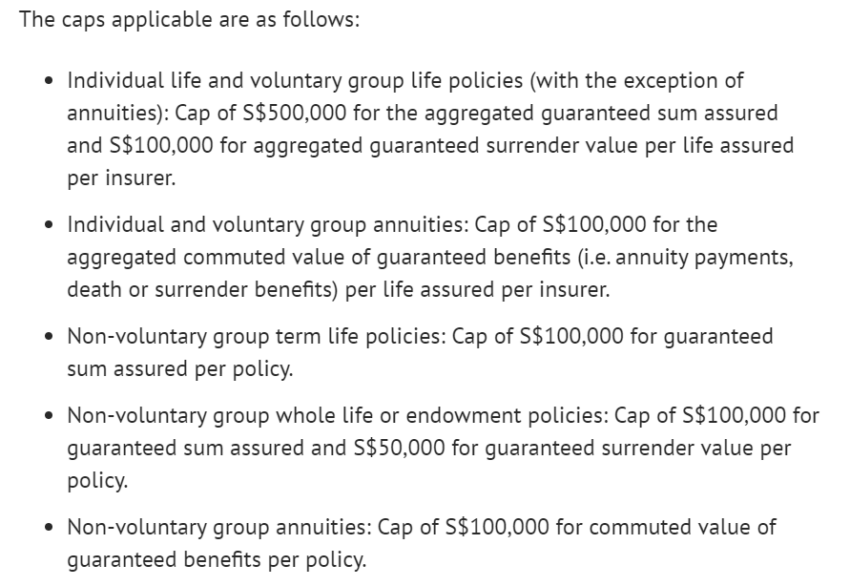

According to SDIC, the benefits payable (such as surrender value) are subjected to certain caps

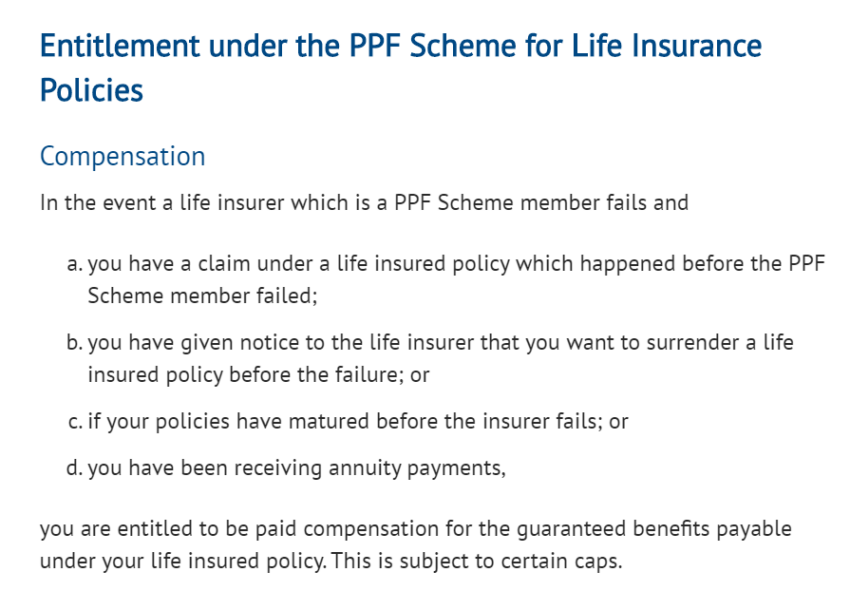

It has also listed 4 scenarios where the insured will be compensated in the event a PPF Scheme member (i.e. Singlife) fails.

In this exhaustive list of scenarios, it is speculated by some that Singlife would fall under scenario d: “you have been receiving annuity payments”. However, it is quickly counter-argued that the ‘interests payments’ seen on the Singlife app should not be considered as annuity payments.

Please be reminded that all such information should not be construed as financial advice. You should seek advice from a licensed representative should you require customised advice on your financial needs. Most of the things you read on the internet are not reviewed by MAS.

The Guidesify team attempted to reach out to Singlife for further clarification but to no avail. Many others have done the same and received no response.

Singlife Referral Bonus 2021

To qualify for the $5 bonus:

1. Download the app + sign up with our link on your mobile

2. Request for a Singlife Visa Debit Card (FREE) on the app

3. Activate the card once received

Bonus: Extra $35 if you sign up for Singlife’s Grow.

Do inform us if you have any form of formal clarification from any of the participating bodies.

At the end of the day, let’s not forget that this scheme only comes into effect if Singlife fails.

Related to Singlife Referral Bonus:

Syfe Promo Code 2020: It Is Not Just REITs